Sorry

http://seekingalpha.com/article/...does-it-really-cost-to-mine-silverZum Artikel:

The silver ETFs (SLV, SIVR, PSLV) and the silver mining equities have had a rough time the past two months, and many investors have just thrown in the towel. However, is now really the time to quit on silver?

One of the key factors that we need to analyze is related to the actual cost of mining silver -- that will help us answer the question if it is time to sell or accumulate SLV.

Introduction

One of the metrics for analyzing any commodity or commodity-based equity (such as the silver miners) is to understand the cost of production -- how much does it actually cost for silver miners to mine silver?

This is very important because unlike gold, industrial demand uses up most silver production. Since about 75% of all new silver supply is mined every year, the actual cost that is involved in mining silver will be very important in determining future supply. If the price is too low, the supply coming from the mines will drop (new projects are curtailed, existing operations are cut, and junior companies simply go out of business), which causes physical silver shortages.

According to the most recent statistics published by the Silver Institute, 2011 silver demand was 1.04 billion ounces, with approximately 877 million ounces used for industrial usage. This silver is needed by the physical market and is used up in production, which makes it much different from gold, since gold is mostly kept as a store of value in societies across the world, while silver serves both the store of value role and is used up in industry. This silver demand is more or less fixed, and as the price goes down, demand may rise as industry stores silver for future production or use more silver as a replacement for other substitutes.

Calculating The True Mining Cost of Silver - Our Methodology

Publicly traded silver companies offer investors a quick non-GAAP formula to give investors a glimpse at their costs per ounce, called "cash costs." This measure may vary slightly from company to company (it is non-GAAP after all), but it is generally their "mining costs" (cost to operate their mines, process silver, pay miners, etc.) divided by the amount of silver equivalent ounces produced. For example, in its 2012 3Q statement, Pan American Silver (PAAS) reported its consolidated cash costs as $13.87 per ounce of silver.

This measure is completely misleading, and selectively reports costs without really giving investors a true picture into the cost it takes to produce silver. If PAAS were truly earning $17.00 per ounce, then its EPS would be much higher than its $38 million reported earnings for the quarter (more along the lines of $100+ million).

The problem is that "cash costs" only include the costs it takes to directly operate the mines, but completely ignores all the other costs of the company, such as administrative costs, royalties, taxes, financing costs, etc. When these costs are included, the true price of silver becomes much higher.

That is why it is important that investors calculate the true costs of silver by adding in all the costs that these companies do not consider "cash costs" and then dividing it by the amount of silver equivalent ounces produced.

Here is how you find the true mining costs for PAAS using the most recent quarter. For the equivalent ounce calculations, I used a gold-to-silver ratio of 50:1, copper-to-silver ratio of 9:1, zinc-to-silver and lead-to-silver ratio of 36:1 -- you may vary it a bit depending on the price of each of those metals you want to use, but it really does not make much difference to the ultimate cost. Also, I have removed a $14 million derivative loss booked by PAAS, since it is not relevant to the actual cost of producing silver (more like a poor bet by management).

As you can see, the real cost of producing an ounce of silver for 3Q 2012 was $24.98, NOT the aforementioned $13.87 -- a much more accurate number for investors to use when analyzing PAAS and the silver market.

So What Are The Industry's TRUE Silver Costs?

The purpose of this article is not to analyze PAAS, but rather, the whole silver industry to determine the cost of producing silver. To do so, I used the methodology that I have shown you above and applied it to as many public silver companies as I could find.

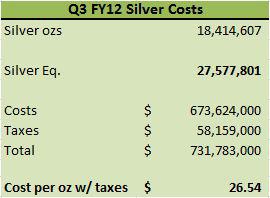

This is what I came up with for 3Q 2012 (the most recent reported quarter), which includes the reported costs of Coeur d'Alene Mines (CDE), Hecla Mining (HL), PAAS, Endeavour Silver (EXK), First Majestic (AG), Silver Standard Resources (SSRI), and Gold Resource Corporation (GORO).

The third quarter production of these companies incorporates 27 million equivalent ounces and comes out to about $26.54 per ounce of silver -- this should be shocking to investors who follow the "cash cost" number offered by silver companies.

Conclusion

Using this information helps us assess our silver investments, which is especially important during this major market downturn. When the true costs of production are so close to the actual silver price, this is a sign that silver is a commodity that needs to be owned -- there really is very little room for it to drop before even producing miners run into serious problems (if they haven't already).

Currently, 4Q 2012 numbers are not out yet for these silver miners (and if you follow me, I will try to post costs as they come in), but most mining executives are facing increasing costs, so I would not be surprised to see the number actually rise.

So SLV investors, steady yourselves and hold tight, because there really is a solid floor for silver at the physical cost level, and what we are seeing now is fund liquidation and shorting (see my article, "COTS Report: Gold Hasn't Been This Shorted Since 2008"). The paper markets are the short-term drivers of silver, but in the end, the physical markets are the true determinants of price.

And IF silver drops below this $26 level (though I don't think it will happen), then buy as much physical silver as you can, because then it may get REALLY interesting when the silver industry starts buying COMEX contracts and asking for delivery because miners are not producing enough (or are not willing to sell at current prices).